Insight

Do ESG hedge funds really exist? Yes, but…

In summary…

- ESG assets rose to $37.8 trillion at year end in 2020[1] and in 2021 (to 31st July), half of European ETF inflows have been to ESG funds.[2]

- The disparate and varied nature of hedge fund strategies and the assets they trade, as well as their ability to short-sell, somewhat ‘muddies the waters’ as far as ESG is concerned.

- Hedge funds that pay proper regard to ESG do exist, but at present, investors need to look ‘under the bonnet’ in order to fully understand, monitor and quantify how ESG is integrated.

- Allocators face several issues in this area of alternative investments, namely:

- greenwashing

- objectives obfuscation

- lack of transparency

- There is a real opportunity cost to the planet from assets flowing to ‘Socially Responsible Investment’ (“SRI”) funds that are not true ESG funds.

The rise of Environmental, Social and Governance (ESG) concerns

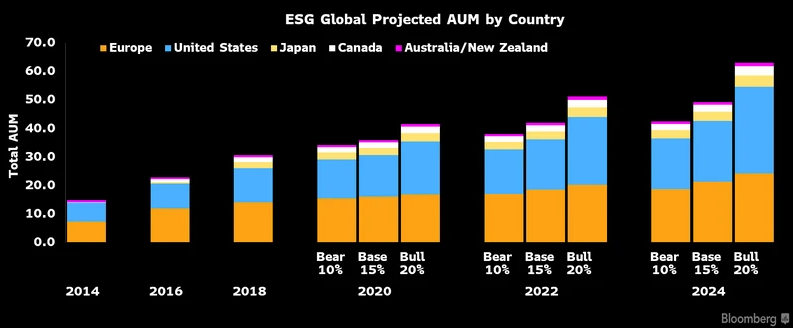

One of the undeniable forces in the investing world in recent years has been the rise of ESG concerns. ESG takes pole position in many asset managers’ marketing materials, mission statements and agendas. Asset flows back up the message; ESG assets across all asset classes rose to $37.8 trillion at year end in 2020[1] and in 2021 (to 31st July), half of European ETF flows have been to ESG funds[2].

Source: GSIA, Bloomberg Intelligence

A growing trend

The trend shows no signs of slowing down. Bloomberg Intelligence estimated earlier this year that ESG assets may account for more than a third of the global total AUM by 2025 (assuming a year on year growth rate of 15% – half the average of the last five years).

ESG-themed hedge funds are on the rise

It is safe to say that ESG is here to stay in asset management and is likely to, if it has not already, permeate most sectors of the industry. Alternative investments, and more specifically, hedge funds, are not immune to this trend.

The disparate and varied nature of hedge fund strategies and the assets they trade, as well as their ability to short-sell somewhat ‘muddies the waters’ as far as ESG is concerned; however, this has not prevented hedge funds from adopting the ESG theme. Funds targeting ESG strategies are commonly described as SRI (Socially Responsible Investment) Funds. Over the last three years, assets designated as SRI, by a large undisclosed hedge fund consultant rose from $75bn in September 2018 to $116bn in August 2021; a 55% increase. This may be due to positive performance and increasing flows to SRI designated funds. It may also be due to an increase in the number of funds re-classifying themselves as SRI.

The questions raised by this growing trend

This increase in SRI designated assets in the hedge fund industry gives rise to a number of fundamental questions, perhaps the most pertinent of which are:

- What exactly is the definition of an ‘SRI hedge fund’?

- What key areas should investors focus upon when considering an allocation to hedge funds whilst fully incorporating ESG considerations?

As part of Aurum’s efforts to answer these questions, we refined the list of funds designated as SRI funds into a smaller peer group of funds that we believe can be defensibly classified as ‘ESG’. SRI is a self-designated title – no independent third party verifies this. Most of these funds stop short of fully including ESG in their investment process or objectives, but implement a simple exclusionary screen at the first stage of defining the investible universe. For Aurum to designate a fund as ‘ESG’, we attempted to do what the new SFDR Article 8 and Article 9 Designation intends to do in July 2022. This entailed examining the funds’ documents detailing investment process and criteria, as well as having conversations with managers to ascertain the extent of ESG involvement. This exercise resulted in the initial SRI peer group which contained 138 funds, managing $116bn in assets, being reduced to just 41 Aurum ESG funds managing $11.3bn in assets – an AUM reduction of 90%.

ESG can be incorporated into hedge funds in numerous different ways. Some of the most common ways are:

Screening

ESG screening finds those companies that score highly (positive screening) and avoiding those that score lowly (negative screening) on ESG factors, relative to their peers

Thematic investing

Aims to identify the most important ESG trends and then use that as the basis for stock-picking; for example, solar energy, online education etc.

Integration

Incorporates ESG information into investment decisions in an effort to enhance risk-adjusted returns

Shareholder advocacy and engagement

This is an activist investment approach in which the fund aims to improve companies’ ESG behaviour/metrics through active engagement with management

Impact investing

Looks to invest in those businesses whose activities will target projects or developments that have a positive, measurable benefit to the environment and/or society, alongside a financial return

Aurum’s analysis highlights some of the issues allocators face in this area of alternative investments, namely:

- greenwashing

- objectives obfuscation

- lack of transparency

The risks of greenwashing

High definition images of the natural world, feel-good messaging, and convincing communication that ESG is ‘integrated in everything we do’… you get the idea.

The process of conveying a false impression or providing misleading information about how a company’s products are more environmentally sound is commonly known as greenwashing. Given the huge inflows to SRI assets, there is likely to be strong temptation for asset managers to be seen to be green.

Greenwashing covers a slew of behaviours, such as cherry-picking certain ESG metrics and the creation of a narrative to market certain funds as ‘ESG-friendly’ or ‘consistent with ESG principles’. At best, many managers appear to be stretching the definition of ESG to the limit when applying it to their fund. At worst, managers are exploiting investors’ preference for ESG, with no real ESG ‘substance’ when one looks closely.

Greenwashing is prominent, not just in regular corporate communication, but also in asset management and hedge funds. In the Asset Management space, we have seen the recent high level exits of individuals such as Tariq Fancy (ex-BlackRock) and Desiree Fixler (ex-DWS Group) who have been vocal about this. Both of these people became concerned about the legitimacy of their employers’ ESG investment products. You can read more on this in Mr Fancy’s recent essay[3] on the matter.

Investors can help to root out greenwashing

Not all funds with a narrative of ESG-alignment, or a broader objective than absolute returns, are necessarily greenwashing. And herein lies the issue: if investors inadvertently allow some funds to greenwash, effectively rewarding these efforts through subscriptions, the issue becomes self-perpetuating. This is due to the fact that funds with more assets have greater resources at their disposal. Bigger funds are also more likely to come onto the radar of large-ticket allocators such as endowments or Sovereign Wealth Funds.

Reliance merely upon ‘SRI’ designation (or some equivalent) allows certain funds to continue to tick boxes and receive assets intended for ESG funds. The more investors reward this, the more incentivised funds are to engage in greenwashing.

The prudent investor should do the requisite due diligence to negate this issue. Reliance merely upon ‘SRI’ designation (or some equivalent) allows certain funds to continue to tick boxes and receive assets intended for ESG funds. The more investors reward this, the more incentivised funds are to engage in greenwashing. However, if investors begin to dig deeper, beyond the marketing, then greenwashing attempts can potentially be identified and thereby may be damaging to the reputation of those involved.

Greenwashing – the risk for true ESG funds

Funds engaging in greenwashing to gain assets are wielding a double-edged sword. They run the risk of investors becoming more knowledgeable and informed about this issue as media focus grows. If this is allowed to persist, investors will eventually act to penalise this action, which is good, since it polices unsubstantiated ESG messaging.

However, this action carries a risk that investors wanting to avoid greenwashing funds could avoid all funds espousing ESG focus. The knock-on effect? Even legitimate ESG funds could lose out on potential assets.

Marketing SRI funds – a lucrative incentive

SRI funds that have gathered assets partly due to their marketing as ESG hedge funds, are cannibalising potential growth of true ESG funds.

Over the last three years, if we examine hedge funds marketed as SRI that have benefited from the flood of asset inflows to ESG funds, we can see that:

- around 88% of performance fees have gone to those SRI funds that do not fall into the category that we believe can be defensibly classified as Aurum ESG hedge funds

- 4% of performance fees generated have gone to funds that fall into a category that we refer to as ‘NEdge funds’, i.e. not exactly hedge funds

- leaving just 8% of performance fees to Aurum ESG hedge funds

This ‘dollar-pie’ of performance fees actually sums to around $2.1bn over the last three years, meaning non-ESG funds picked up around $1.9bn in performance fees alone.

There is a real opportunity cost for the planet

Some of the true ESG funds have an ‘impact’ element to their return objective. This could be through direct investment in companies best positioned to combat the largest ESG issues and furthering the UN’s Sustainable Development Goals[4] (UN SDGs).

Less investment towards effecting change in the world and potentially advancing the UN SDGs

Consider a $10m investment intended for an ESG hedge fund. If that $10m is allocated to a fund that isn’t a true ESG fund, then that is a $10m opportunity cost reducing investment towards effecting change in the world and advancing the UN SDGs.

In the second part of this series, we examine the obfuscation of investment objectives commonly observed in this segment of the hedge fund industry.

-

https://www.bloomberg.com/professional/blog/esg-assets-may-hit-53-trillion-by-2025-a-third-of-global-aum/

-

https://mondovisione.com/media-and-resources/news/trackinsight-esg-etfs-capture-50-of-european-flows-in-historic-2021/

-

https://medium.com/@sosofancy/the-secret-diary-of-a-sustainable-investor-part-1-70b6987fa139

-

The UN ‘Sustainable Development Goals’, or SDGs, are a set of 17 interconnected global goals, established in 2015 with a target achievement date of 2030, intended as a “blueprint to achieve a better and more sustainable future for all”.

All figures and charts use asset weighted returns unless otherwise stated. All data is sourced from Aurum Hedge Fund Data Engine.

Disclaimer

This Post represents the views of the author and their own economic research and analysis. These views do not necessarily reflect the views of Aurum Fund Management Ltd. This Post does not constitute an offer to sell or a solicitation of an offer to buy or an endorsement of any interest in an Aurum Fund or any other fund, or an endorsement for any particular trade, trading strategy or market. This Post is directed at persons having professional experience in matters relating to investments in unregulated collective investment schemes, and should only be used by such persons or investment professionals. Hedge Funds may employ trading methods which risk substantial or complete loss of any amounts invested. The value of your investment and the income you get may go down as well as up. Any performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable indicator of future results. Returns may also increase or decrease as a result of currency fluctuations. An investment such as those described in this Post should be regarded as speculative and should not be used as a complete investment programme. This Post is for informational purposes only and not to be relied upon as investment, legal, tax, or financial advice. Whilst the information contained in this Post (including any expression of opinion or forecast) has been obtained from, or is based on, sources believed by Aurum to be reliable, it is not guaranteed as to its accuracy or completeness. This Post is current only at the date it was first published and may no longer be true or complete when viewed by the reader. This Post is provided without obligation on the part of Aurum and its associated companies and on the understanding that any persons who acting upon it or changes their investment position in reliance on it does so entirely at their own risk. In no event will Aurum or any of its associated companies be liable to any person for any direct, indirect, special or consequential damages arising out of any use or reliance on this Post, even if Aurum is expressly advised of the possibility or likelihood of such damages.

Share this article with your network

Share with your network