Hedge Fund Data

Hedge fund industry performance deep dive – H1 2024

Download full report

In summary…

- Hedge funds ended H1 2024 up 6.1%, outperforming bonds, -3.2%, but behind equities, +9.2%

- Quant was the strongest performing master strategy in H1, +8.7%, after being the weakest master strategy in 2023

- Arbitrage is the worst performing strategy, delivering +2.1% in H1, after being the second-worst strategy in 2023

- Industry AUM grew, albeit marginally, in the first half. This growth was largely driven by P&L; all strategies had negative net flows except multi-strategy and quant

- Alt UCITS underperformed hedge funds in all strategies, with the exception of long biased alt UCITS which delivered 6.2% v 5.5% for long biased hedge funds

Contents:

Strategy chart packs

Hedge fund industry performance review

Asset growth

Hedge fund assets – as measured by those funds reporting to Aurum’s Hedge Fund Data Engine – have grown by $103.1bn since the end of 2023 to stand at just under $3.0tn. This was driven by net positive performance (+$149.4bn) and partially offset by outflows (-$46.3bn). All eight hedge fund master strategies saw net growth in AUM, led by equity l/s, followed by quant. Equity l/s growth was driven by positive P&L, which was partially offset by sizeable investor outflows. Quant growth in AUM was exclusively driven by significant net positive P&L, which was offset by moderate net investor outflows. Long biased was the strategy which experienced the largest net investor outflows, but this was offset by net positive P&L.

About Aurum

Aurum is an investment management firm focused on selecting hedge funds and managing fund of hedge fund portfolios for some of the world’s most sophisticated investors. Aurum also offers a range of single manager feeder funds.

Aurum’s portfolios are designed to grow and protect clients’ capital, while providing consistent uncorrelated returns. With 30 years of hedge fund investment experience, Aurum’s objective is to lower the barriers to entry enabling investors to access the world’s best hedge funds.

Aurum conducts extensive research and analysis on hedge funds and hedge fund industry trends. This research paper is designed to provide data and insights with the objective of helping investors to better understand hedge funds and their benefits.

CHANGE IN AUM (YTD)

Headline performance

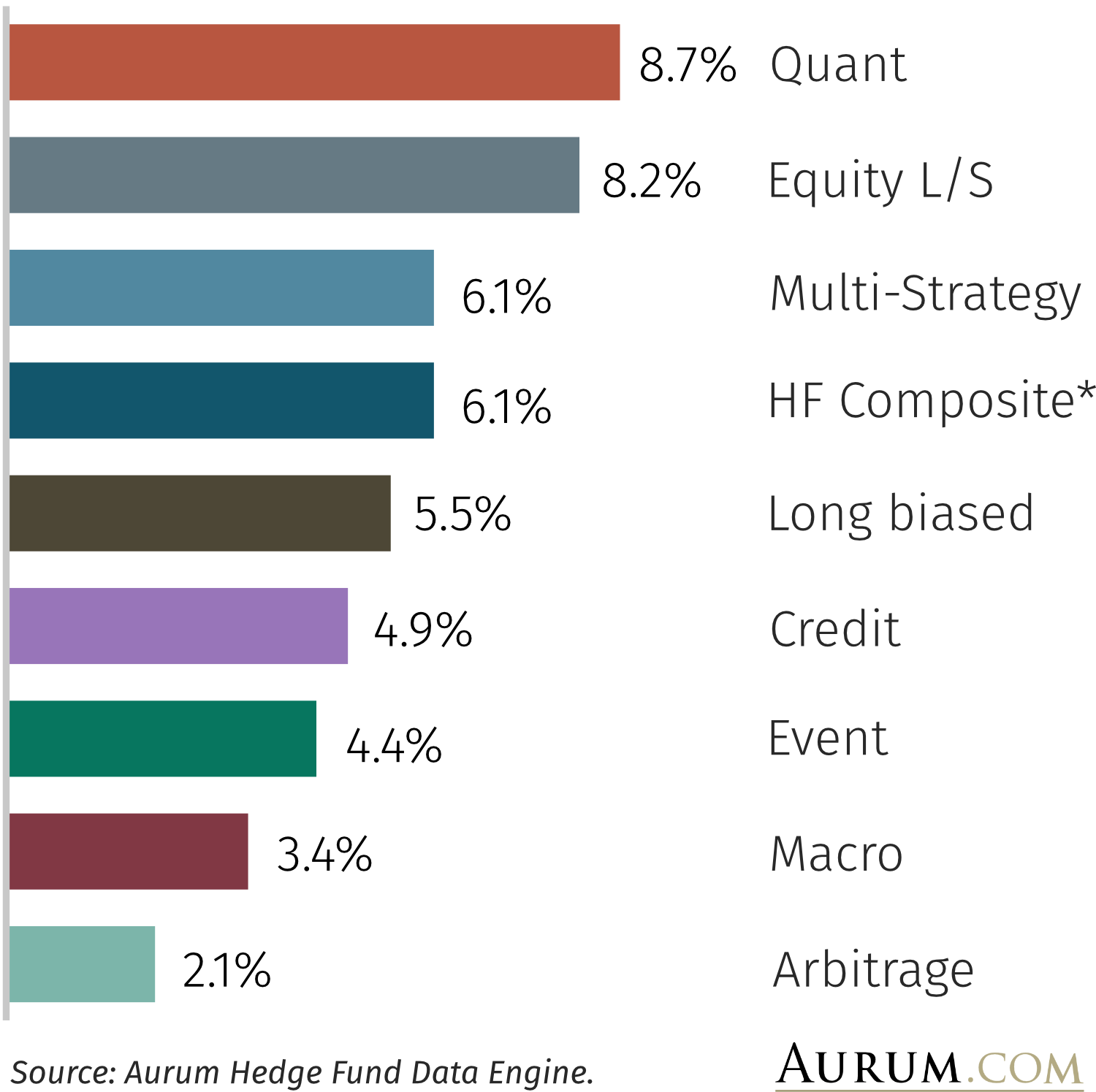

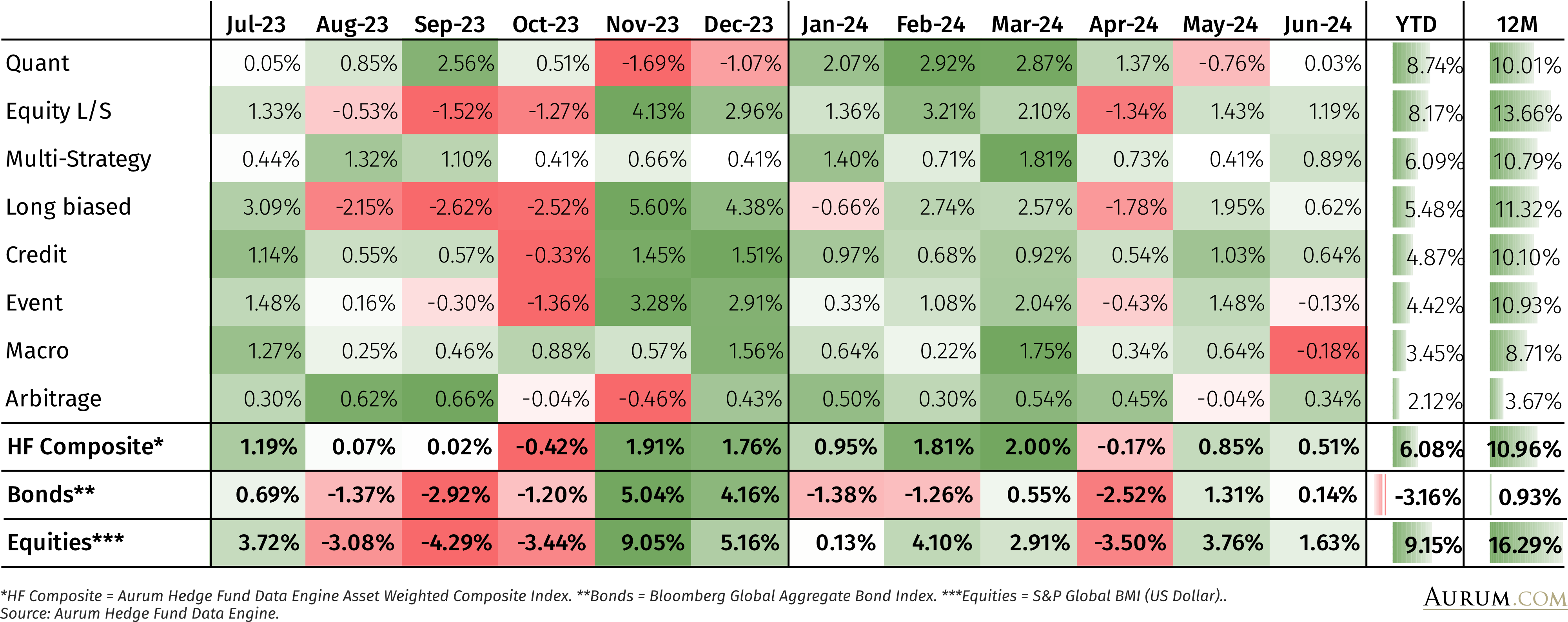

The hedge fund industry was up 6.1% for the first half of 2024 (on an asset weighted basis). This compares to the mean figure of 5.9%, suggesting that, on average, larger hedge funds have outperformed. The median performing hedge fund returned 4.5% for the year. The median performing hedge fund sub-strategy was event – activist (ranked 19th out of 37 sub-strategies returning +4.9%). The largest constituent of the hedge fund universe was equity long/short (“equity l/s”) (~21% of assets), followed by multi-strategy and long biased – each constituting ~14%. Quant was the strongest performing strategy returning 8.7% on an asset weighted basis.

NET RETURN (YTD)

Strong equity markets supported the performance of strategies highly correlated to those markets. The industry headline figure was dragged down by underperformance from arbitrage, macro, event and credit.

Quant, equity l/s (+8.2%) and multi-strategy (+6.1%) outperformed the industry average. The industry headline figure was dragged down by underperformance from arbitrage (+2.1%), macro (+3.5%), event (+4.4%) and credit (+4.9%). Long biased (+5.5%) funds were marginal underperformers relative to the HF Composite figure.

Strong equity markets supported the performance of strategies highly correlated to those markets such as equity l/s – APAC (11.6%), equity l/s – US (+8.2%), equity l/s – sector (+8.0%), equity l/s – global (8.0%) and equity l/s – EUR (+7.6%). With the exception of equity l/s – APAC, these were all sub-strategies which were among the top performers in 2023. This strong performance from equity markets was not without volatility, which created a supportive environment for strategies like quant – multi (+10.3%), quant – EMN (+9.2%) and quant – stat arb (+8.6%).

At the other end of the performance table, arbitrage – tail (-1.6%) is the only sub-strategy to have negative performance in the first half of 2024. The strongest performing sub-strategy in 2023, event – activist, which made over 20% in 2023, is now underperforming the industry average in H1 2024, +4.9%.

The majority of positive performance in the first half of 2024 was concentrated in Q1. The hedge fund composite performance in Q1 was 4.8%, whereas in Q2 it was just 1.2%. April (-0.2%) was the weakest month year-to-date in both bond and equity markets (down 2.5% and 3.5% respectively) and was the only down month year-to-date for the hedge fund composite. The negative industry performance that month was driven by those strategies more correlated to risk assets (long biased, equity l/s and event).

Five-year performance (CAR) for hedge funds now stands at 6.4%, comfortably outperforming bonds (-2.0%) but underperforming equities (+8.3%) from a total return perspective, however, outperforming equities from a risk-adjusted perspective (Sharpe of 0.7 vs 0.4).

Dispersion

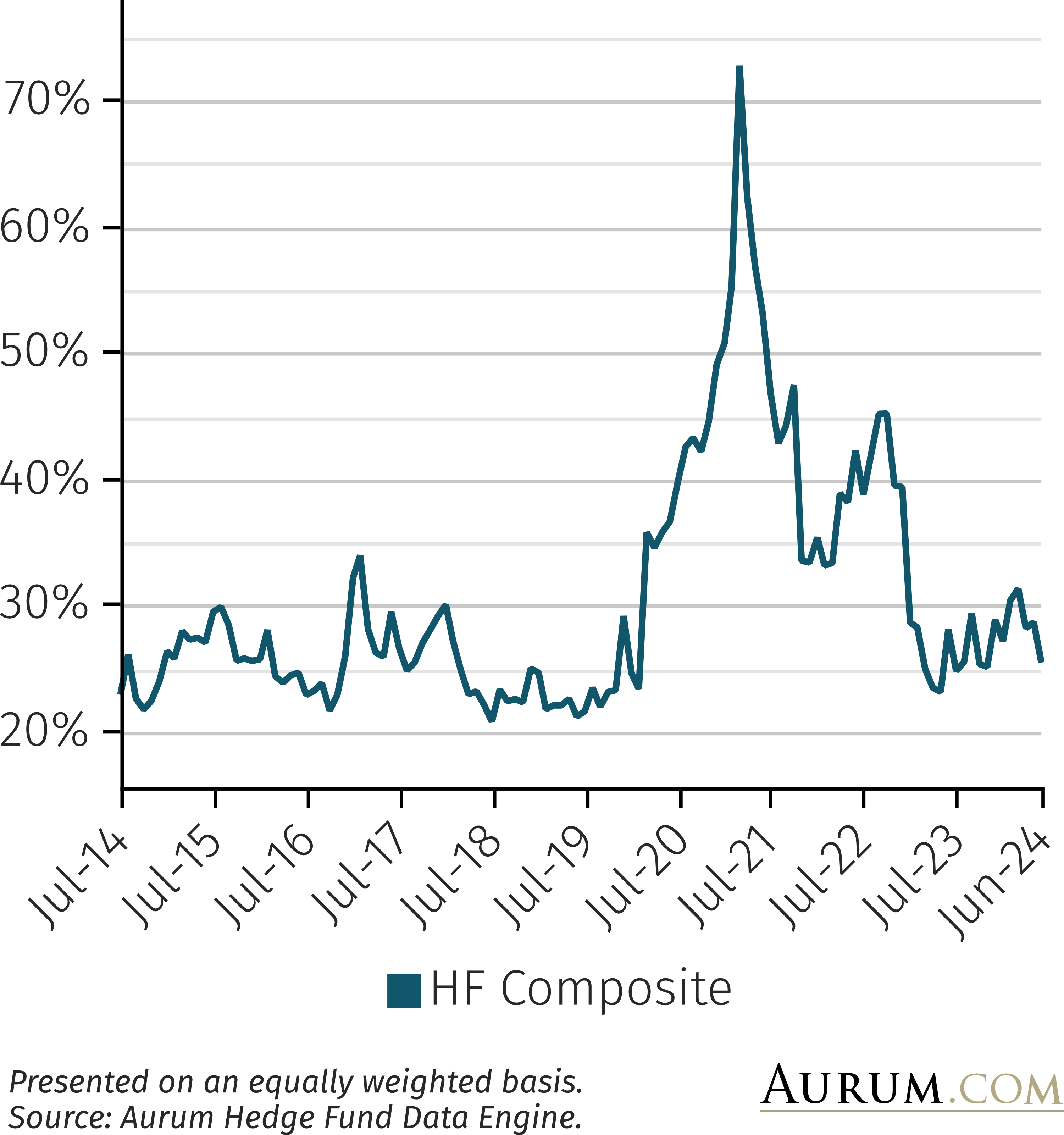

As can be seen in the following chart, dispersion between top and bottom decile performing hedge funds has fallen from the dramatic levels seen during the peak markets’ disruption caused by COVID. Since early 2023 it has been more in line with dispersion levels observed pre-COVID. Since the prior report, dispersion in performance across the hedge fund industry has fallen. As can be seen on page 21 of industry report, the fall in performance dispersion has occurred across the majority of hedge fund master strategies and all sit below their ten-year average levels. However, it’s important to note that these ten-year averages are influenced by the heavy distortions caused by the COVID-19 pandemic.

10th – 90th PERCENTILE 12M ROLLING PERF. SPREAD[1]

STANDARD DEVIATION (1 YR)

Strategy performance

Quant is the top performing headline strategy with a number of its sub-strategies among the top performers.

As indicated above, some of the top performing strategies in H1 2024 have been those that have sub-strategies that exhibited a higher correlation and a material beta to equities, or are able to capitalise on elevated levels of volatility in markets. Quant is the top performing headline strategy (+8.7%) with a number of its sub-strategies among the top performers, including quant – multi (+10.3%), quant – RP (+9.9%), quant -macro (+9.4%), quant – EMN (+9.2%), and quant – stat arb (+8.6%). Equity l/s (+8.2%) has been driven by some of the top performing sub-strategies, including equity l/s – APAC (+11.6%), equity l/s – US (+8.2%), equity l/s – sector (+8.0%), equity l/s – global (+8.0%) and equity l/s – EUR (+7.6%). Multi-strategy funds have also outperformed the broader hedge fund universe and have been long-term consistent performers (5y CAR of +10.5% with a Sharpe of 2.1).

The worst performing strategy was arbitrage (+2.1%), driven by underperformance from the arb – tail sub-strategy (-1.6%) and from arb – vol (+0.8%). It is no surprise that tail hedging strategies would once again underperform in 2024 given the negative beta associated with the strategy and declining realised and implied volatility levels when compared with 2020, which was an outstanding year for the strategy. Arb – vol strategies have historically performed better in negative, volatile, market environments. Macro (+3.5%) was the second worst performing master strategy – it struggled due to relative underperformance from macro – global (+3.0%) and macro – FIRV (+3.1%).

NET RETURN OF MASTER STRATEGIES (1 YR)

-

Presented on an equally weighted basis. Source: Aurum Hedge Fund Data Engine.

*HF Composite = Aurum Hedge Fund Data Engine Asset Weighted Composite Index.

**Bonds = Bloomberg Global Aggregate Bond Index.

***Equities = S&P Global BMI (US Dollar).

All figures and charts use asset weighted net returns unless otherwise stated. All Hedge Fund data is sourced from Aurum Hedge Fund Data Engine. Data included in this report is dated as at 15th July 2024.

The Hedge Fund Data Engine is a proprietary database maintained by Aurum Research Limited (“ARL”). For information on index methodology, weighting and composition please refer to https://www.aurum.com/aurum-strategy-engine/. For definitions on how the Strategies and Sub-Strategies are defined please refer to https://www.aurum.com/hedge-fund-strategy-definitions/

Bond Index

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Bloomberg does not approve or endorse this material or guarantee the accuracy or completeness of any information herein, nor does Bloomberg make any warranty, express or implied, as to the results to be obtained therefrom, and, to the maximum extent allowed by law, Bloomberg shall not have any liability or responsibility for injury or damages arising in connection therewith.

Equity Index

The S&P Global BMI (the “S&P Index”) is a product of S&P Dow Jones Indices LLC, its affiliates and/or their licensors and has been licensed for use by Aurum Research Limited. Copyright © 2021 S&P Dow Jones Indices LLC, its affiliates and/or their licensors. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC. For more information on any of S&P Dow Jones Indices LLC’s indices please visit www.spdji.com. S&P® is a registered trademark of Standard & Poor’s Financial Services LLC and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC. Neither S&P Dow Jones Indices LLC, Dow Jones Trademark Holdings LLC, their affiliates nor their third party licensors make any representation or warranty, express or implied, as to the ability of any index to accurately represent the asset class or market sector that it purports to represent and neither S&P Dow Jones Indices LLC, Dow Jones Trademark Holdings LLC, their affiliates nor their third party licensors shall have any liability for any errors, omissions, or interruptions of any index or the data included therein.

By accepting delivery of this Paper, the reader: (a) agrees it will not extract any index values from the Paper nor will it store, reproduce or further distribute the index values to any third party for any purpose in any format or by any means except that reader may store the Paper for its personal, non-commercial use; (b) acknowledges and agrees that S&P own the S&P Index, the associated index values and all intellectual property therein and (c) S&P disclaims any and all warranties and representations with respect to the S&P Index.

Share this article with your network

Share with your network